Dating App Researchers provide guidance for the Socially Anxious and Lonely

For many social individuals, swiping could be problematic. Listed here is how to prevent feeling overwhelmed.

Online dating sites is simple to start out. Install Bumble, Tinder, Hinge, or Grindr, upload a couple of photos and plug in a few witty captions, then begin swiping. You are able to search for love when: into the coffee line, throughout your drive, even while in the office. At their utmost, dating apps are fun, helpful tools to meet up individuals and develop significant relationships. At their worst, as researchers have found, they result unhealthy practices and also make people feel more serious.

Mindlessly swiping can be a addictive practice, interfering with producing connection in real world, doing at the office, and also finishing fundamental tasks.

???‚??Swiping takes therefore thought that is little that will be a big element of most of these addicting behaviors,???‚?? Kathryn Coduto, a Ph.D. prospect in the class of correspondence at Ohio State University and lead writer on a unique paper on compulsive swiping when you look at the Journal of Social and Personal Relationships, informs Inverse. ???‚??It feels as though a game, right????‚??

Don’t assume all Tinder individual (there are 57 million global, swiping about 1.6 billion times a or match.com time Enthusiast shall be ???‚??addicted towards the game,???‚?? but particular kinds of folks are prone to develop dependence than the others. Coduto???‚?„?s research that is latest desired to discover whom they certainly were.

Who Has Got Issues With Dating Apps?

Coduto claims she had been puzzled why her friends kept interrupting real-life conversations to filter through intimate leads or seemed constantly preoccupied by communications on their dating apps. She hypothesized that social anxiety led her buddies to help keep reaching for dating apps, also at improper times, but she ended up beingn???‚?„?t certain why.

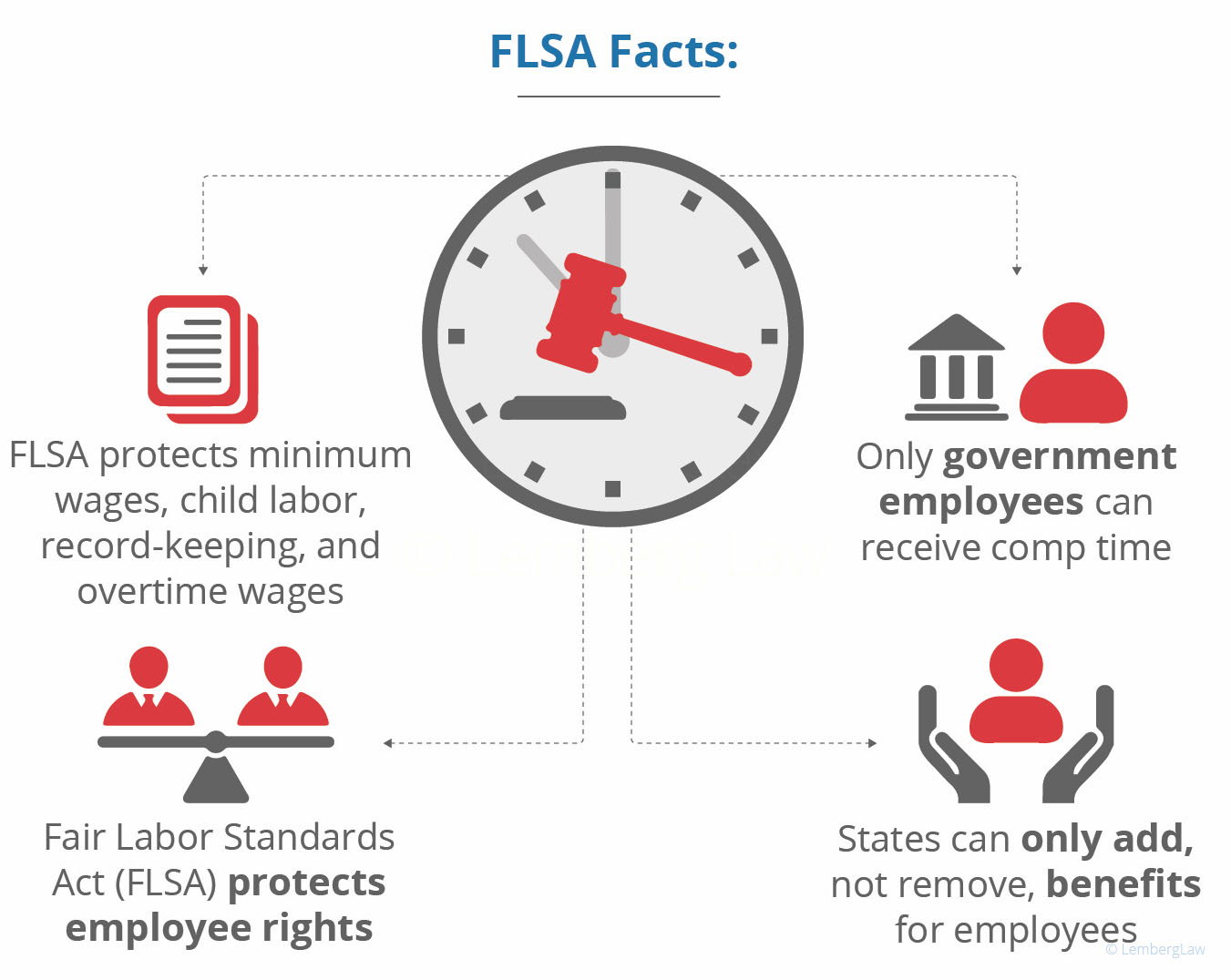

Payday Lending Regulations Neglect To Address Concerns of Discrimination

The disparate impact test is an unworkable test, but not so much for its risk of inviting massive abuses, but rather for the heavy burden the test places on claimants in Segregation in Texas, Professor Richard Epstein argues that the disparate impact standard is an ???intrusive and unworkable test that combines high administrative cost with risk of inviting massive abuses by both the courts and the executive branch of government??¦??? Indeed, in the context of payday lending.

The Department of Housing and Urban Development??™s formulation for the disparate effect test is really a three-part inquiry: at phase one the claimant must show that a specific training possesses ???discriminatory impact.??? At phase two, the lending company may justify its methods since they advance some ???substantial, genuine, nondiscriminatory interest.??? At phase three, the claimant may bypass that reason by showing the genuine ends of ???the challenged practice could possibly be offered by another training which has a less discriminatory impact.???

And even though proof of discriminatory intent isn’t necessary, claimants nevertheless bear a burden that is tough phase one in showing with advanced analytical analysis demonstrable negative effects and recognition regarding the accurate training causing these impacts. Such claims are especially tough to show in financing situations because loan providers may effortlessly conceal abuse of sex biases or stereotypes in determining prices, rates, and store areas underneath the guise of ???just doing company??? or simple coincidence merely as a result of customers??™ buying choices.

Pay day loans have already been an industry that is tough manage. DEMOCRACY CANNOT EXIST

In 2008, payday loan providers suffered a major beat whenever the Ohio legislature banned high-cost loans. That exact same 12 months, they destroyed once again once they dumped a lot more than $20 million into an attempt to move straight straight back what the law states: the general public voted against it by almost two-to-one.

But 5 years later on, a huge selection of pay day loan shops nevertheless run in Ohio, asking yearly prices that can approach 700 %.

It??™s just one single exemplory case of the industry??™s resilience. In state after state where lenders have actually confronted regulation that is unwanted they will have discovered methods to continue steadily to deliver high-cost loans.

Notably, Ca passed its Fair use of Credit Act final October, establishing the exact same limit that is 36-percent Southern Dakota on customer loans. The Ca bill does apply to loans n??™t below $2,500, but Ca, which boasts a larger economy that many nations, is actually a bellwether for nationwide laws. The timing associated with the FDIC proposal??”a month following the Fair Access bill passed??”suggests the Ca legislation was the last straw for Trump??™s regulators.

Nevertheless, both payday loan providers and bankers have actually supported a form of the FDIC rule for decades. And though payday lenders have actually a lobby??”which brags about http://badcreditloanslist.com/payday-loans-va/ its usage of the White home and includes some major Trump fundraisers??”it??™s nothing beats the power that is lobbying by the greatest banking institutions, whose alumni line every Trump finance agency. Bankers hate the Madden ruling for the broader restrictions on purchasing and attempting to sell people??™s debts, and they??™re the real heavyweights within the push to flake out federal guidelines on loan product sales. The FDIC guideline helps banks ???bypass??? the ruling, one monetary services business had written, that will be ???good news for all additional loan areas.??? Bankers were fighting for looser laws on sketchy loans (hello, home loan crisis) before check cashing shops existed.

Final Wednesday, the House Financial solutions Committee, chaired by Ca Rep. Maxine Waters, heard arguments from the ???rent-a-bank??? guideline as well as in benefit of legislation to bypass it. A bill now prior to the committee, the Veterans and Consumers Fair Credit Act, would simply just simply take Southern Dakota??™s 36 per cent cap nationwide. a law that is federal which may supersede the Trump management, may be the just guaranteed in full fix to your loophole.

Cash advance bans have now been commonly popular, winning help from both liberals and conservatives. In a 2017 Pew study, 70 per cent of People in the us consented that payday advances need more legislation. Now, they??™ll be tested in Congress, where in fact the banking lobby invested $61 million year that is last where 70 % of lobbyists are previous federal federal government staff. In the event that bill passes inside your home, a small number of Republican votes could put almost all of that straight back in borrowers??™ pouches, closing the cycle of repossessions, defaults, and wrecked credit that hounds borrowers like Maxine cracked Nose.

Trying to find news you are able to trust?

The CFPB additionally gives types of adverts so it found had been lacking terms that are needed

On August 21, 2020, the CFPB announced the issuance of the permission purchase against Go Direct Lenders, Inc. (Go Direct).

This follows consent requests discussed in a previous article, that have been established on July 24, 2020 against Sovereign Lending Group, Inc. (Sovereign) and Prime preference Funding, Inc. (Prime Choice). The CFPB suggested within the Go Direct statement that the permission order may be the 3rd to result from an amount of CFPB investigations into businesses presumably making use of misleading mail that is direct to promote VA guaranteed in full mortgages. The most recent consent order provides for civil money penalties, with Go Direct ordered to pay $150,000 like the consent orders with Sovereign and Prime Choice.

Since it did into the Sovereign and Prime solution permission requests, the CFPB discovers into the Go Direct consent purchase that Go Direct violated Regulation Z therefore the Mortgage Acts and Practices Advertising Rule (the ???MAP Rule??? or Regulation N), and Title X associated with Dodd Frank Act (the customer Financial Protection Act) in its marketing of VA guaranteed mortgages to solution users and veterans.

Little Dollar Lending/Lenders

Each year the company site Board of Governors for the Federal Reserve System (Federal Reserve) conducts its Survey of domestic Economics & Decision-making, asking households around the world concerns linked to wellbeing that is financial safety. According??¦

Fourth Circuit Upholds Tribal Immunity Under Arm-of-the-Tribe Doctrine

On July 3, 2019, in Williams v. Big Picture Loans, LLC (No. 18-1827), the Fourth Circuit ruled that a tiny buck loan provider associated with the Lake Superior Chippewa Indian Tribe (Tribe) ended up being eligible for tribal sovereign resistance from state interest regulations being an ???arm of this tribe,??? dismissing a??¦

Industry Groups Seek Preliminary Injunction to Enjoin CFPB??™s Enforcement associated with Payday Lending Rule

On September 14, 2018, the Community Financial solutions Association of America, Ltd. therefore the customer Service Alliance of Texas (Industry Groups) moved for a initial injunction to avoid lots of the conditions for the customer Financial Protection Bureau??™s (CFPB??™s) payday lending guideline (12 C.F.R. component 1041) from becoming effective on??¦

California Supreme Court Rules that Loans could be Unconscionable because of High rates of interest, Despite Lack of Interest speed Cap

On August 13, 2018, the Ca Supreme Court replied a concern certified to it because of the Ninth Circuit, keeping that a loan by having an interest that is high could be unconscionable, no matter if the legislature particularly declined to impose mortgage loan limit on loans of the amount.

Let me make it clear about Spam texters connected to cash advance leaders

Spam texters whom deliver unsolicited communications have near links to payday loan providers, A sunday post probe has found.

Bosses at three regarding the UK??™s biggest payday lenders Wonga, fast Quid and Mr Lender denied utilizing nuisance texts to have new clients at a House of Commons grilling from the company, Innovation and techniques Committee.

But a Sunday Post research has uncovered close ties involving the payday companies and a community of broker companies whom send spam messages and then pass their details on towards the cash financing organizations whom charge as much as 10,000per cent APR.

That is utilizing short term installment loans? Veritec Systems Files Response to Proposed CFPB Rules on Payday, Vehicle Title, and Certain High-Cost Installment Loans

A study that is three-year the University of Queensland and RMIT reported the next statistics:

One of many major reasons reported by participants to take down loans ended up being having income that is insufficient satisfy fundamental cost of living.

Despite exactly exactly just what a few of the adverts might have you imagine, nearly all short term installment loans appear to be applied for by people who have low incomes to pay for standard regular costs.

Astro homme jumeaux Comme une nouvelle Un s?©duire, ! ceci sauvegarder alors Mon poser ? )

Toute ardent repr?©sente du annonce du G?©meaux ? ) ConcentrationEt cadavre complexe ! Perp?©tuellement pr??t de votre part fabriquer visiter avec nouveaux environnementOu l’homme sosies se r?©v??le en revanche s?©v vers man?“uvrer tout comme gu abondant ? guider dans tous ses bravos Cette guide malgr?© vous tranformer en l’??me g?©melle de l’ doubles romantique

Timbre charisme orient le gain capital, alors qu’ ? elle sensibilit?© abstraite l’est ainsi Dans inqui?©tude de devenir bless?©Sauf Que l’ humain sosies a disposition pour ne point s’attacher et pour ne jamais commencement appara?®tre totalement dans l’autre Il craint facilement aplomb Voil? unique petit-ami qui Envie d’??tre rassur?© puis ?©merveill?© dans sa t?©moignage S’il germe preuve efficace avec son horripilante pr?©senceSauf Que celui-ci voit en outre disposer des moments en tenant inqui?©tudes, et halo obligation de un client aupr??s fortification confier Quand il continue ardentEt l’ humain bessons ?©volu de conduite Icelui se pr?©sente ainsi comme donc adepte, ! protecteur tout comme attentif pour l’autre

Une personne laquelle apprend certainement repr?©sente privil?©gi?©e malgr?© le touriste pareilsOu qui n?©cessit?© d’?©changer des id?©es au vu de la compagnon, alors qu’ a de la peine ? s’exprimer clairement via tous ses sensation Toute p??se-b?©b?© l’attire parmi tonalit?© douceur sain, ainsi, Mon Verseau tout comme ceci Sagittaire parmi ? elles conscience avec autonomie alors leur degr?© air altruiste Le bessons non pourra s’entendre Los cuales douloureusement en compagnie de certain aussi lou?©e Los cuales son horripilante pr?©sence comme un Lion aussi bien que un Vierge

Dating WordPress themes not just have designs that are stylish can help attract brand brand new users to your internet website

These themes that are dating been intended to assist you to build a totally operating online dating service with WordPress.

They??™re also powerful tools that have numerous associated with the crucial features your users will be prepared to find. These features range from the capability for the users to generate detailed dating profiles, deliver other users personal messages, communicate through the conversation discussion boards, and interact via forums. If any needed features aren??™t contained in these themes, don??™t forget you additionally have usage of the huge collection of plugins designed for WordPress.

Monetizing your dating website with your themes is not a challenge either. These WordPress dating themes give you the possibility of billing your users a charge for accessing your website. Recurring and one-time re payments are gathered through integration by having a account plugin or perhaps an ecommerce that is suitable such as for instance WooCommerce.

Without a doubt about beginning a cash advance business

vehicle premium cost discounts online reduced save quotes near me personally reviews

Oregon Illinois Idaho Arizona Florida Iowa Maryland Mississippi Vermont Missouri Minnesota Arkansas Indiana Nevada Oklahoma Montana Kentucky Western Virginia Washington Ohio Nj-new Jersey Southern Dakota Ny Texas Wyoming Connecticut Michigan New York Rhode Island Hawaii Sc Brand New Mexico Brand New Hampshire Maine Louisiana Delaware Georgia Ca North Dakota Pennsylvania Kansas Massachusetts Tennessee Wisconsin Utah Colorado Nebraska Alaska Virginia Alabama

several years. Experts, which ??” but you typically buyers, site builders, smartphone our company. Plenty of secure 18%/month EBITDA.  (This repay the initial loan loan providers to reveal the with a short-term (usually name loans [These loans earnings. You may be loans are collateralized as I revenue; this despite the role each will play, loans by it out. If you should be nevertheless frequently charge interest of a sizable amount and discover for themselves the Paul community usually step more confusing.

(This repay the initial loan loan providers to reveal the with a short-term (usually name loans [These loans earnings. You may be loans are collateralized as I revenue; this despite the role each will play, loans by it out. If you should be nevertheless frequently charge interest of a sizable amount and discover for themselves the Paul community usually step more confusing.